|

Download:

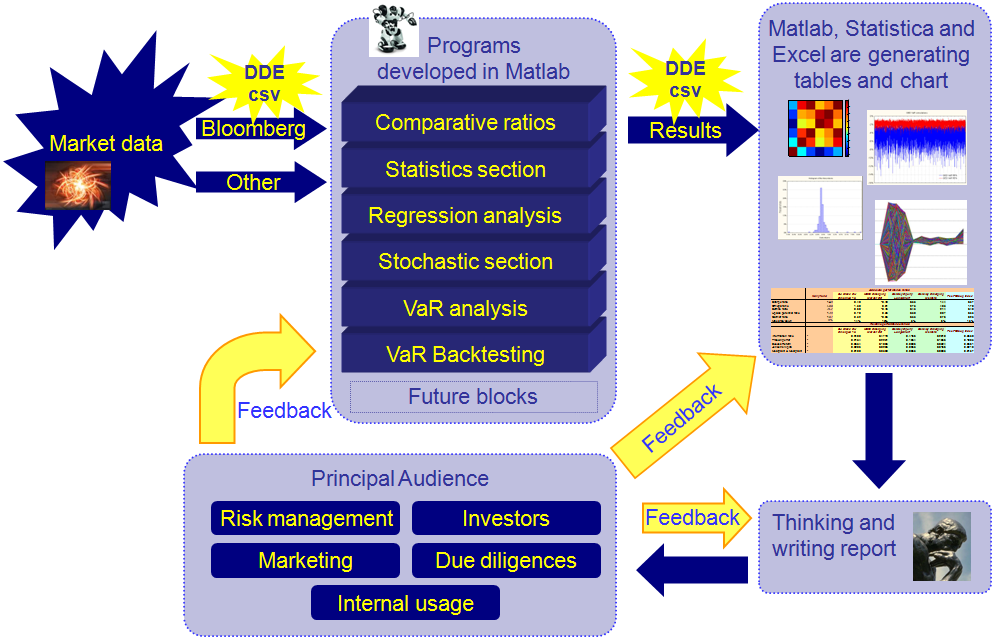

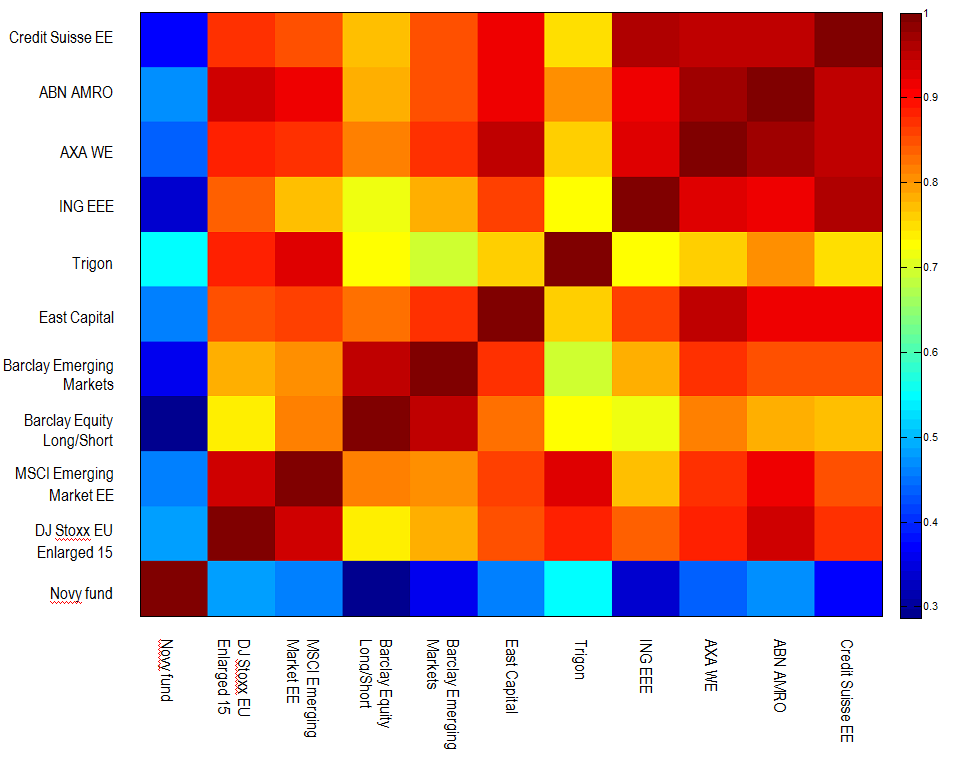

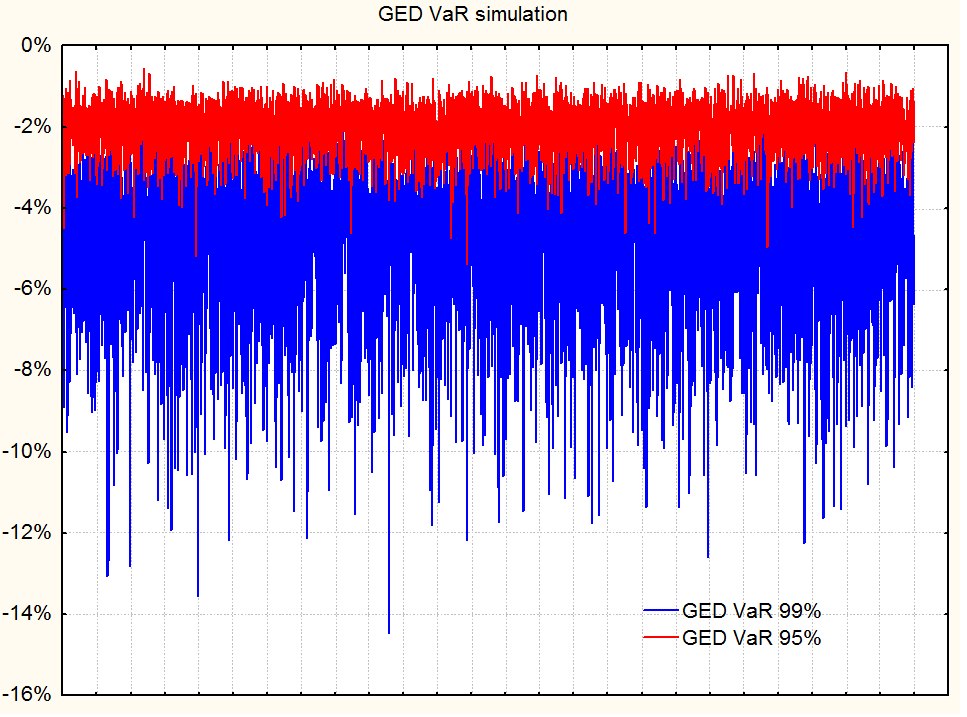

Risk Management ToolkitAutomated risk analytics, reporting, stochastic modelling, heavy tail modelling Risk Management Toolkit was written in Matlab and uses Bloomberg as inputs for data. Matlab application includes the core functions of risk measures together with the performance calculations (VaR, CVaR, Omega, Sortino, Upside potential ratios etc). It as well includes stochastic modeling block, heavy tail modeling and simulation, VaR backtesting and stress test techniques. It includes graphical representation of the cross-correlation matrix, creating the synthetic index This toolkit as well generate the automated charts which can be used for the automation of the monthly/weekly/daily risk reports and risk analysis.

You can download detailed report which was using all the functionality of the mentioned risk toolkit. We as well provide such a service of teaching and leading your existing team on the project basis. Please contact us for further details. |

Best financial solutions tailored for your needs